Media Contacts: Chris Gilroy & Brian Gilroy | WildLife Partners

High-income earners face a specific problem: when income spikes in a single year, the tax bill can be enormous-and the wrong response can be just as costly as doing nothing. The right approach is not aggressive tax theater. It is structured, documented, CPA-aligned planning that uses legitimate strategies to legally reduce taxable income without creating audit exposure.

This guide covers the most effective tax reduction strategies available in a high-income year, who they apply to, and how to implement them cleanly.

What Causes a High-Income Year?

A high-income year usually happens when income arrives in an unusually large amount or in a different form than normal. That can create a much higher tax bill than expected—especially if planning starts too late.

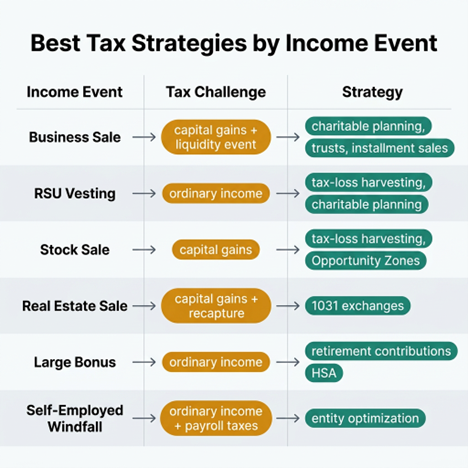

Business Sale:

Quick answer: If you’re selling a business, planning should happen before the transaction closes. Capital gains planning, charitable giving, entity review, installment sale planning, and state tax planning are often most effective before liquidity occurs.

Selling a business can create a major tax event involving capital gains, depreciation recapture, installment planning questions, and state income tax exposure. For entrepreneurs, this is one of the most critical moments for pre-sale planning.

Large Bonus or Commission: A strong year in sales, finance, medicine, or executive compensation can create a spike in ordinary income. Because bonuses and commissions are taxed as ordinary income at the highest marginal rates, the income tax impact can be immediate and substantial.

Stock Sale or RSU Event: Stock sales, RSU vesting, and option exercises can create either ordinary income, capital gains, or a mix of both depending on timing and structure. These events often catch high income earners off guard because the tax treatment is not always intuitive.

Real Estate Exit: Selling appreciated real estate may trigger capital gains, depreciation recapture, state income tax, and decisions around reinvestment, installment treatment, or 1031 exchange eligibility. Rental properties with significant accumulated depreciation present a particularly complex picture.

Inheritance or Windfall: Some windfalls do not create income tax immediately, while others do. The tax treatment depends on the source, structure, and what happens after the assets are received.

Deferred Compensation Payouts: Deferred compensation can create concentrated taxable income in one year-especially for executives and high income professionals whose plans distribute at a fixed schedule.

Event | Tax Character |

Business sale | Capital gains / ordinary income |

Bonus year | Ordinary income |

RSU vesting | Ordinary income |

Stock sale | Capital gains |

Property sale | Capital gains / recapture |

Deferred comp payout | Ordinary income |

Why Waiting Until Year-End Is a Mistake

The biggest mistake in a high-income year is assuming tax planning can wait until the fourth quarter.

By the time income is recognized, many of the best options are already limited. Deadlines may be missed. Certain structures take time to implement correctly. And when planning happens too late, investors end up reacting to a federal income tax bill instead of shaping it.

That late-stage scramble usually leads to reactive decisions, missed deductions, poor CPA coordination, and reduced flexibility. The strongest tax reduction strategies are put in place before the income event—not after the tax problem becomes urgent.

The best time to think about lowering future tax bills is before a high-income year begins. Future tax bills compound the problem when early opportunities are missed.

Tax Savings Through Real Estate: Depreciation, Cost Segregation, and Bonus Depreciation

Real estate remains one of the most powerful categories of tax savings available to high income earners and high income professionals. Unlike most investments, qualifying real estate can generate income while simultaneously creating deductions that offset that income-producing tax savings that are both legal and well-documented.

Real Estate Depreciation and Real Estate Professional Status

Real estate depreciation allows qualifying property owners to deduct portions of an asset over time to reduce taxable income. For investors who qualify as a real estate professional under IRS rules, depreciation losses from rental properties may be used to offset ordinary income rather than being limited to passive loss rules. Real estate professional status is a significant designation—it requires meeting specific hour and participation thresholds-but for qualifying investors, it is one of the most valuable tax benefit opportunities available.

Rental properties generate depreciation that can reduce more taxable income year over year, and when combined with cost segregation, the early-year impact becomes even more substantial.

Cost Segregation

Cost segregation accelerates depreciation by identifying shorter-life property components within a real estate asset. Rather than depreciating everything over one long schedule, a cost segregation study may move fixtures, site improvements, and specialty systems onto faster schedules-accelerating deductions into earlier years when they matter most. This is particularly valuable in a high-income year when the goal is to reduce taxable income quickly and efficiently.

Bonus Depreciation

Bonus depreciation allows qualifying taxpayers to accelerate deductions into the current tax year, sometimes providing a near-immediate deduction in the year of purchase. When available under current law, bonus depreciation can significantly increase near-term deductions for qualifying assets. Because treatment has changed across tax years and may continue to shift, this should always be reviewed with a CPA for the specific asset and tax year involved.

Tax-Loss Harvesting and Capital Gains Tax Planning

Tax-Loss Harvesting

Tax-loss harvesting involves selling losing positions in taxable investing accounts to offset capital gains-one of the most accessible tax reduction strategies for investors with investment portfolios. Done well, tax-loss harvesting can offset capital gains from selling stock, RSU vesting events, or other realized gains, reducing the capital gains tax owed in a high-income year.

The strategy is straightforward in concept but works best when coordinated early and implemented carefully to avoid wash sale issues, poor portfolio decisions, or unintended consequences for qualified dividends and other income. Tax-loss harvesting is most powerful when it is part of a year-round discipline-not a year-end scramble.

Capital losses that exceed current-year gains may carry forward to offset future capital gains, providing ongoing tax savings beyond the current tax year.

Paying Capital Gains Taxes Strategically

Paying capital gains taxes is unavoidable in many high-income years—but the rate you pay depends on holding period, income level, and tax year. Long-term capital gains receive favorable tax treatment compared to ordinary income, with rates that vary based on modified adjusted gross income and filing status. Investors who cross certain income thresholds may also face the net investment income surtax, which adds an additional layer on top of federal income tax for investment income.

Strategic decisions around when to recognize gains-timing income across tax years, deferring where possible, and pairing gains with losses—can meaningfully reduce paying capital gains taxes in any single year.

Charitable Giving: Donor Advised Funds, Appreciated Assets, and Fair Market Value

Donor Advised Funds

Charitable giving is one of the most flexible and powerful tools for high income earners in a high-income year. Donor advised funds allow investors to contribute appreciated assets-stock, real estate, or other property-and receive a potential immediate deduction at fair market value without triggering capital gains tax on the appreciation. The assets are then invested inside the donor advised fund and distributed to public charities over time.

This structure can be especially useful in a high-income year because it allows investors to bunch multiple years of charitable giving into a single year, maximize the itemized deduction impact, and still control the timing of actual grants to charitable organizations. To save charitable, high earners should prioritize contributing in peak-income years when the deduction is worth the most.

Avoid structures where charitable giving is combined with a defined contribution plan masquerading as a tax shelter-these arrangements have drawn IRS scrutiny and rarely survive audit review.

Appreciated Asset Donations and Fair Market Value

Donating appreciated assets directly to qualified charities allows investors to deduct the fair market value of the asset while avoiding paying capital gains taxes on the built-in appreciation. This is one of the most tax efficient ways to give-save charitable high earners who are already planning to give can dramatically improve outcomes by contributing appreciated assets rather than cash.

The fair market value deduction applies to publicly traded securities and certain other assets, subject to adjusted gross income limitations that a CPA can help navigate.

Private Foundations

Private foundations offer a similar framework for investors with larger charitable objectives, though they come with more administrative requirements and different deduction limitations than donor advised funds. For families planning significant multi-generational philanthropy, they can be worth evaluating alongside simpler structures.

Federal Income Tax Brackets, Adjusted Gross Income, and Why They Matter

Understanding Federal Income Tax and Tax Brackets

Federal income tax is calculated on taxable income-which is adjusted gross income minus deductions. Understanding where your income falls within the federal tax brackets is foundational to all high-income year planning, because the marginal rate on additional income can be 37 percent or higher when factoring in federal taxes, state income tax, and the net investment income surtax.

Tax brackets are not a cliff-income is taxed at each rate only for the portion of income that falls within that bracket. But for high income earners, a significant portion of income is often taxed at the top federal income tax rate, which is why strategies that reduce adjusted gross income-not just gross income-matter most.

Adjusted Gross Income and Modified Adjusted Gross Income

Adjusted gross income is the figure that determines eligibility for many deductions, credits, and planning strategies. Modified adjusted gross income is a related calculation used in specific contexts-including Roth IRA contribution eligibility, the net investment income tax, and certain credit phase-outs.

For high income earners, reducing adjusted gross income is often the most powerful lever available, because it opens up access to deductions that would otherwise phase out and lowers the baseline against which federal income tax is calculated. Strategies that reduce adjusted gross income include retirement contributions, health savings account contributions, self employment tax deductions, and certain business deductions. Every dollar of reduced adjusted gross income reduces the overall tax burden-including exposure to surtaxes that phase in at higher income levels.

Earned income-wages, salaries, and self-employment income-is subject to both income taxes and payroll taxes, which is why entity structure and retirement contribution decisions matter especially for high income professionals with significant earned income.

W-2 Income and Tax Strategies for Employees

W-2 Income Planning

W-2 income is the most constrained income type from a tax planning perspective. Employees cannot deduct ordinary business income expenses the way business owners can, and they have fewer structural levers available. But that does not mean high income W-2 earners are out of options.

The most effective strategies for W-2 income earners include:

- Maximizing 401(k) and defined contribution plan contributions to reduce adjusted gross income

- Contributing to a health savings account for triple-tax advantages

- Using a traditional IRA or Roth IRA depending on income level and future tax expectations

- Strategic charitable giving through donor advised funds

- Tax-loss harvesting in taxable investing accounts

- Dependent care tax credit and child tax credit where eligible

- Reviewing whether itemized deductions exceed the standard deduction

For W-2 earners with large equity compensation, the planning extends further-covering RSU timing, option exercise strategy, and whether income can be shifted across tax years to avoid stacking all of it into a single peak year.

401(k), Defined Contribution Plans, and Retirement Accounts

401(k) and Defined Contribution Plan Contributions

Retirement accounts remain one of the cleanest and most familiar ways to reduce current taxable income. A 401(k) or other defined contribution plan allows employees and business owners to contribute pre-tax dollars that reduce adjusted gross income immediately-dollar for dollar. For high income earners in peak earning years, maximizing these contributions should be a first step before evaluating more complex strategies.

A defined contribution plan contribution reduces taxable income in the year it is made. For business owners, a solo 401(k) or SEP-IRA can support significantly larger contributions than a standard employee plan, creating even larger reductions in adjusted gross income.

Do not forget business expenses and plan contributions that are easy to overlook in a high-income year-these are often the biggest tax deduction opportunities hiding in plain sight.

Roth IRA, Traditional IRA, and Strategic Conversion Planning

A traditional IRA contribution may reduce taxable income today—subject to income limits and whether the investor has access to a workplace retirement plan. A Roth IRA contribution does not reduce current federal taxes, but it grows tax free and allows tax-free withdrawals in retirement. For investors who expect to be in higher tax brackets later, a Roth IRA may provide better lifetime tax savings even without an upfront deduction.

A Roth IRA conversion-moving funds from a traditional IRA or tax deferred account into a Roth IRA-means paying income taxes now in exchange for tax free withdrawals and then tax-free withdrawals of earnings in retirement. This strategy works best in years when income is lower than usual, allowing investors to convert at a lower federal income tax rate. In a high-income year, conversions are generally less attractive, but a CPA can help model the lifetime tax savings tradeoff.

Health Savings Account Strategies

Health Savings Accounts and Triple-Tax Advantages

A health savings account is one of the most tax efficient vehicles available and is often underused in broader tax planning. Contributions to a health savings account are deductible above the line—reducing adjusted gross income regardless of whether you itemize. Growth inside the account is tax deferred, and qualified withdrawals for medical expenses are tax free. That combination of deductible contributions, tax deferred growth, and tax-free withdrawals makes it one of the few truly triple-tax-advantaged tools in the tax code.

Health insurance premiums paid out of pocket and other qualified medical expenses can be covered with health savings account distributions tax free. For high income earners who can afford to pay current medical expenses out of pocket, allowing the health savings account to grow as a tax deferred account provides compounding tax savings over time.

College savings accounts-specifically 529 plans-offer a similar structure for education expenses, with after-tax contributions growing tax free and allowing tax-free withdrawals for qualified education expenses. The American opportunity tax credit is another education-related tool worth evaluating, particularly for families with qualifying students.

Tax-Efficient Strategies for Business Owners and Self-Employed Professionals

Business Expenses, Payroll Taxes, and Entity Optimization

Business owners have significantly more flexibility than W-2 employees in a high-income year. Ordinary business income can be offset by a wide range of legitimate business expenses-and forget business expenses that are properly documented is one of the most common and costly mistakes business owners make. Every legitimate business expense reduces taxable income dollar for dollar.

Self employment tax applies to net self-employment income and represents a significant cost for high income professionals who are not structured through an entity. The self employment tax deduction-equal to half of the self employment tax paid-reduces adjusted gross income and provides partial relief. Payroll taxes, including the employer share paid through a business entity, can also affect planning decisions around how to structure compensation.

Pay payroll taxes efficiently by reviewing entity structure with a CPA. An S corporation structure can allow a business owner to take a reasonable salary-subject to payroll taxes-while taking additional income as distributions not subject to self employment tax or payroll taxes. This distinction matters significantly for high income professionals with large ordinary business income.

Rental Properties and Tax Reduction Strategies

Rental properties remain one of the most effective tax reduction strategies for business owners and investors alike. Beyond depreciation, rental real estate can generate losses that-depending on the investor’s participation level and real estate professional status-may offset other income. Understanding the passive activity rules, the real estate professional status designation, and how rental properties interact with modified adjusted gross income thresholds is essential to capturing the full tax benefit available.

Defined Contribution Plan and Retirement Planning for Business Owners

A defined contribution plan-including a solo 401(k), SEP-IRA, or defined benefit plan-can allow business owners to make very large retirement contributions that reduce taxable income immediately. In high income years, these contributions are often the single biggest tax deduction available to self-employed professionals and business owners. Maximizing defined contribution plan funding before year-end should be a standard step in any high-income year planning process.

Tax-Free and Tax-Deferred Strategies

Tax-Deferred Retirement Accounts and Tax-Free Growth

Tax deferred retirement accounts-including traditional IRAs, 401(k) plans, and SEP-IRAs-reduce taxable income today and allow growth to compound without annual federal taxes on investment returns. Tax dollars that would otherwise go to the IRS stay invested and compound over time, which can represent significant lifetime tax savings.

Tax free growth is available through Roth accounts, health savings accounts, and certain college savings accounts. For high income earners, strategically balancing tax deferred accounts and tax-free accounts-based on current and expected future tax brackets-is a key component of long-term tax planning.

Opportunity Zones and Tax Deferral

Opportunity Zone investments may allow investors with eligible capital gains to defer paying capital gains taxes while potentially improving after-tax outcomes when held long enough and structured correctly. These should be evaluated based on both tax treatment and asset quality-not just the tax angle. For investors in a high-income year with significant realized gains, Opportunity Zones may provide a legitimate deferral vehicle if the underlying investment meets quality standards.

1031 Exchanges

A 1031 exchange allows qualifying investors to defer capital gains tax through reinvestment. Instead of triggering immediate capital gains on the sale of qualifying real estate, investors may defer those taxes by reinvesting into another qualifying property under applicable rules. The 1031 exchange is one of the most well-established and CPA-supported tax reduction strategies available to real estate investors.

Itemized Deductions, Property Taxes, and Other Often-Overlooked Tax Breaks

Itemized Deductions vs. Standard Deduction

For high income earners with significant deductible expenses, itemized deductions can produce better outcomes than the standard deduction. Eligible itemized deductions may include state income tax and property taxes (subject to the SALT cap), mortgage interest (only the interest portion is deductible, not principal), charitable contributions, and certain medical expenses above the threshold.

The state tax deduction-combined with property taxes-can add up meaningfully for investors in high-tax states, though the current cap on state and local tax deductions limits this lever for many high earners. A private mortgage insurance deduction may also be available in certain situations.

Property Taxes and State Income Tax

Property taxes and state income tax represent real costs that belong in any high-income year tax analysis. In states with high income tax rates, state income tax can represent a significant portion of total tax dollars paid. While the federal deduction for state and local taxes is capped, some states offer a state tax deduction for contributions to certain retirement plans or charitable vehicles, which can provide partial relief.

Child Tax Credit, Dependent Care Tax Credit, and Education Credits

Several credits can lower your tax bill directly-reducing tax liability dollar for dollar rather than simply reducing taxable income. The child tax credit applies to qualifying children and begins to phase out at higher income levels. The dependent care tax credit may apply to qualifying childcare and dependent care expenses. The American opportunity tax credit applies to qualifying education expenses for eligible students.

These credits are worth reviewing even for high income earners, as income thresholds and phase-out rules vary and do not always eliminate eligibility entirely.

How Wealthy Investors Plan Before a Big Tax Event

Tax-Efficient Pre-Event Planning

High income professionals and wealthy investors rarely wait until the money hits their account to start planning. Instead, they focus on pre-sale planning, CPA coordination, entity planning, charitable planning, and liquidity preparation. The pattern is consistent: they do not chase a last-minute loophole. They build a plan early enough that their options are still open.

The goal is not to eliminate taxes entirely-it is to reduce unnecessary tax exposure in a tax efficient manner while keeping strategy compliant, defensible, and aligned with long-term wealth goals. A lower tax bill achieved through careful, documented planning is far more durable than one achieved through aggressive structures that create audit risk.

Lower your tax bill strategically by focusing on strategies with real economic substance—real estate depreciation, retirement contributions, charitable giving, and entity structure-rather than manufactured deductions or promoter-driven schemes.

Tax Strategies That Often Trigger Red Flags

Some tax strategies sound sophisticated but create more risk than value. Common red-flag areas include aggressive trust structures, fake write-offs, offshore gimmicks, conservation easement abuse, and promoter-driven schemes. These arrangements often rely on vague legal theories, exaggerated marketing, or paperwork that does not reflect real economic substance.

The Internal Revenue Service has repeatedly scrutinized abusive tax structures, especially when promoters oversell deductions or understate audit risk. Strategies that promise to eliminate more taxable income than seems plausible, or that cannot be clearly explained to a CPA, are almost always a signal to slow down.

Serious investors-including the WildLife Partners audience-tend to prefer strategies that are understandable, documented, and coordinated with qualified professionals rather than sold as shortcuts. The question to ask is not “Does this lower my tax bill?” but “Can this lower my tax bill in a way my CPA would defend?”

Common Mistakes During High-Income Years

The biggest tax planning mistakes are predictable:

Waiting too long. The most expensive mistake is often not paying taxes-it is losing the planning window. Reduce taxable income-remember that many strategies require action before year-end or before the income event itself. Once the income is recognized, many options close. When high income years stack on top of each other, the compounding tax burden makes early action even more important.

Chasing tax shelters. Investors who lose money in a bad investment because it promised a big tax break have paid twice: once in poor returns, and once in audit exposure.

Ignoring adjusted gross income. Many valuable deductions and credits phase out at certain modified adjusted gross income thresholds. Reducing adjusted gross income is often more valuable than chasing a deduction further down the return.

Forgetting payroll taxes and self employment tax. For business owners and self-employed professionals, these represent a significant portion of total federal taxes and belong in the planning conversation.

No CPA review. Tax reduction strategies work best when coordinated with a qualified CPA who understands the investor’s full picture-income type, state income tax exposure, entity structure, and long-term objectives.

High-Income Year Tax Checklist

Use this as a practical planning framework:

✅ Estimate federal income tax and state income tax exposure early

✅ Review capital gains and whether tax-loss harvesting applies

✅ Max 401(k) and defined contribution plan contributions

✅ Evaluate health savings account funding and contribution limits

✅ Review charitable giving strategy—donor advised funds, appreciated assets

✅ Assess real estate and depreciation opportunities

✅ Evaluate Roth IRA conversion feasibility in the context of current tax brackets

✅ Review entity structure and business expenses

✅ Consider Opportunity Zone or 1031 exchange options for real estate exits

✅ Coordinate with CPA before year-end-not after

Final Takeaway

A high-income year is not a crisis-it is a planning opportunity. The goal is not to eliminate taxes entirely. It is to legally reduce unnecessary tax exposure while keeping your strategy compliant, defensible, and aligned with long-term wealth goals.

The most effective tax reduction strategies in a high-income year are almost always the least dramatic: plan early, work with your CPA, document everything, and use strategies grounded in real economic value. Whether that means maximizing a defined contribution plan, donating appreciated assets to a donor advised fund, harvesting capital losses, or investing in real estate for depreciation-the thread is the same. Lower your tax bill through structure, not shortcuts.

For the right investor, proactive planning in a high-income year can produce meaningful lifetime tax savings-tax dollars preserved through legitimate strategy that compound alongside the rest of the portfolio. That is what CPA-backed, red-flag-free tax planning actually looks like.

Frequently Asked Questions

How do I reduce taxes during a high-income year?

High income earners usually reduce taxes through depreciation, charitable giving, retirement contributions, tax-loss harvesting, capital gains planning, and CPA coordination. Start early-the best options close once income is recognized.

How can I offset capital gains legally?

Through tax-loss harvesting, charitable giving of appreciated assets at fair market value, Opportunity Zone investments, 1031 exchanges for qualifying real estate, and other strategies tied to timing and asset structure.

Can charitable giving reduce taxes?

Yes-especially through donor advised funds or direct donations of appreciated assets. The tax benefit depends on the asset, fair market value, timing, and adjusted gross income.

What tax deductions work best for high earners?

The biggest tax deduction opportunities typically come from retirement contributions, real estate depreciation, business expenses, charitable planning, and real asset strategies. The right fit depends on whether the income is W-2 income, business income, or investment income.

Can real estate reduce taxable income?

Yes. Qualifying real estate can reduce taxable income through depreciation, cost segregation, and bonus depreciation. Real estate professional status may allow losses from rental properties to offset ordinary income.

What is tax-loss harvesting?

Selling positions at a loss in taxable investing accounts to offset capital gains elsewhere. Losses that exceed current-year gains may carry forward to future tax years.

What tax strategies trigger red flags?

Vague trust structures, fake write-offs, abusive easements, offshore gimmicks, and promoter-driven schemes that promise large deductions without clear economic substance. If a strategy cannot be explained clearly to a CPA, that is a warning sign.

What should I do before a liquidity event?

Estimate federal income tax and state income tax exposure early, coordinate with your CPA, evaluate charitable and reinvestment options, review entity structure, and document decisions before the transaction closes.

Are Roth IRA conversions useful in high-income years?

Generally less attractive in high-income years because conversions are taxed at peak tax brackets. They tend to work better in lower-income years, but a CPA can model the lifetime tax savings tradeoff.

What is a health savings account and how does it help?

A health savings account offers deductible contributions, tax deferred growth, and tax-free withdrawals for qualified medical expenses-one of the most tax efficient savings vehicles available for high income earners.

Disclosures:

The content published on the 1776ing Blog is for informational and educational purposes only and should not be considered financial, legal, tax, or investment advice. The insights shared are intended to promote discussions within the alternative investment community and do not constitute an offer, solicitation, or recommendation to buy or sell any securities or investment products.