Rental income is the heartbeat of real estate investing for accredited investors—those with a net worth over $1 million (excluding their primary residence) or annual income exceeding $200,000 ($300,000 joint)—but not all properties deliver the cash flow you deserve. A single-family rental limping along at $20,000 a year on a $1 million investment, bogged down by vacancies, repairs, or outdated leases, can sap your financial momentum. What if you could sell that lackluster earner, reinvest the proceeds into a property generating two or three times the rental income, and defer the capital gains taxes that typically take a bite out of your profits? That’s the power of a 1031 exchange, a tax-deferred strategy under Section 1031 of the Internal Revenue Code. This comprehensive guide zeros in on how accredited investors can use a 1031 exchange to upgrade their rental income, transforming modest returns into robust cash flow streams. With Great Point Capital’s Alternative marketplace streamlining the process, you can unlock higher rental income—whether through traditional rentals or passive Delaware Statutory Trusts (DSTs)—and keep your capital working harder, tax-free.

Why Rental Income Matters for Accredited Investors

Rental income isn’t just a nice-to-have—it’s a critical metric for accredited investors seeking steady, predictable returns from their real estate portfolios. Unlike speculative appreciation, rental income provides cash flow you can count on month after month, fueling reinvestment, debt service, or personal financial goals. A property netting $20,000 annually on a $1 million investment (2% yield) might barely cover its own costs, let alone generate meaningful income, while one producing $60,000 (6%) delivers real earning power. Yet, upgrading to a higher-income rental by selling often means facing capital gains taxes—20% federally, plus state rates (e.g., 13.3% in California)—that shrink your proceeds. A 1031 exchange eliminates this barrier, letting you reinvest every dollar into properties that maximize rental income. IPX1031 calls this a way to “enhance cash flow,” a priority for high-net-worth individuals aiming to optimize their rental portfolios.

How a 1031 Exchange Upgrades Rental Income

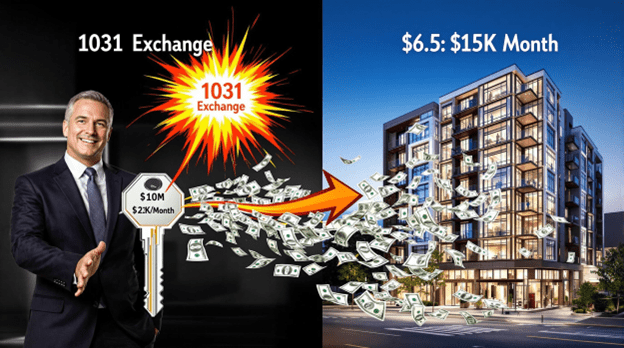

A 1031 exchange allows you to sell an investment property and reinvest the proceeds into a “like-kind” replacement—any U.S. real estate held for investment—without paying immediate capital gains taxes. The focus here is rental income: by swapping a low-yield property for one with higher rental returns, you boost your cash flow while deferring taxes. Here’s how it works:

Swap for Higher Yields

Trade a 2% rental ($20K/year on $1M) for a 6% rental ($60K/year on $1M), tripling income. This could mean selling a single-family home in a saturated market with declining rents and buying a well-leased multifamily property in a growth city like Raleigh, where occupancy rates and rental demand are soaring. The tax deferral ensures you’re not losing $100,000–$200,000 of your proceeds to the IRS, letting you fully fund a property that delivers robust monthly cash flow. For accredited investors, this upgrade can turn a trickle of rental income into a steady torrent, amplifying returns without dipping into personal capital.

Consolidate for Efficiency

Sell multiple low-income rentals and buy one high-income property, like a multifamily with strong leases. Imagine unloading three $500K rentals—each netting just $10K/year due to sporadic tenants and upkeep—and exchanging into a $1.5M apartment building with a 6% yield ($90K/year), anchored by long-term renters. This not only slashes management time from juggling multiple properties to overseeing one but also leverages economies of scale, as larger rentals often command higher per-unit rents and lower per-unit costs. It’s a streamlined path to rental income dominance, keeping your tax-deferred proceeds fully invested in a single, high-performing asset.

Shift to Passive Rentals

Reinvest into a DST, where institutional-grade properties deliver 4–6% rental income, paid passively. Instead of managing a $1M rental yielding $20K/year with constant tenant headaches, you could exchange into a DST stake in a $25M commercial complex, netting $50K/year without lifting a finger, thanks to professional sponsors handling operations. These properties—think Class-A office towers or multifamily jewels—often boast stable, creditworthy tenants, ensuring consistent rental checks mailed to you monthly. For accredited investors, this shift upgrades rental income while freeing up time, with Great Point Capital’s Alternative marketplace.

The tax deferral is the kicker: a $1 million sale with a $400,000 gain might lose $120,000 to taxes (30% combined rate), leaving $880,000. With a 1031 exchange, you keep the full $1 million, amplifying your ability to secure rentals with superior income potential replacement properties.

The Mechanics: Turning Low Rents into High Returns

The 1031 exchange process is straightforward but rigid: use a Qualified Intermediary (QI) to hold sale proceeds, identify replacements within 45 days, and close within 180 days. The “like-kind” rule offers flexibility—exchange a single-family rental for a multifamily, a retail space with tenants, or a DST stake—as long as it generates rental income for investment purposes. The goal is clear: leverage your untaxed proceeds to acquire properties that elevate your rental cash flow, whether through higher rents, better occupancy, or lower overhead.

Step-by-Step: Upgrading Your Rental Income with a 1031 Exchange

Here’s a precise roadmap to boost your rental income via a 1031 exchange:

- Assess Current Rental Income: Review your portfolio’s performance—e.g., a $1M rental yielding $20K/year (2%) after vacancies and repairs. Calculate net income, not just gross rents, to spot underperformers. Pinpoint properties with stagnant or declining rental returns begging for an upgrade.

- Set Rental Income Targets: Aim high—e.g., 5–7% ($50K–$70K/year on $1M)—based on market benchmarks. Consider tenant stability, lease terms, and maintenance costs to ensure sustainable cash flow. This goal drives your exchange strategy.

- Engage a QI: Hire a reputable QI (e.g., IPX1031’s team) to hold proceeds securely, ensuring tax deferral. Their expertise keeps you compliant, critical when chasing higher rental income with big dollars at stake.

- Sell the Low-Income Property: Market your underperformer—say, a $1.5M rental netting $30K/year (2%)—and sell, coordinating with your QI to escrow funds. Speed matters to maximize your 180-day window.

- Explore High-Income Options with Great Point Capital’s Alternative Marketplace: Use Great Point Capital to source rentals with robust yields—multifamily units, leased commercial spaces, or DSTs. Its tools connect you to listings and sponsors, simplifying the hunt for cash-flow kings.

- Identify Replacements (45 Days): List properties within 45 days—e.g., a $1.5M multifamily at 6% ($90K/year). Target variety or focus on one high-income gem, ensuring rental upside. Submit your list via your QI.

- Close Within 180 Days: Finalize purchases, matching or exceeding the sold property’s value to defer all gains. Your QI releases funds, locking in your new, higher rental income stream.

Real-World Examples: Rental Income Upgrades

- Scenario 1: Single-Family to Multifamily Boost

You own a $1M single-family rental in Tampa yielding 2% ($20K/year) after tenant churn. You sell, deferring a $300K gain, and exchange into a $1.5M multifamily in Raleigh with 6% ($90K/year) from stable leases. Result? $70K more rental income annually, tax-deferred. - Scenario 2: Scattered Rentals to Commercial Cash Cow

Four $500K rentals in Detroit total $2M, netting $40K/year (2%) with spotty tenants. You sell via a 1031 exchange and buy a $2M retail center in Nashville, fully leased at 5.5% ($110K/year). Outcome? $70K rental income jump, one property to oversee. - Scenario 3: Active Rental to Passive DST

A $1.8M apartment building in Seattle yields 3% ($54K/year) but demands constant attention. You exchange into a DST stake in a $36M multifamily, deferring $600K in gains, netting 5.5% ($99K/year) passively. Gain? $45K more rental income, no management.

The DST Advantage: Passive Rental Income Powerhouse

For accredited investors, Delaware Statutory Trusts (DSTs) redefine rental income potential within a 1031 exchange. Inland Private Capital highlights DSTs as “institutional-quality properties”—e.g., a $50M apartment complex—delivering 4–6% rental yields ($40K–$60K on $1M) via monthly distributions. Professional sponsors handle leasing and upkeep, so your rental income flows without effort. Swap a $1M active rental at 2% ($20K/year) for a DST at 5% ($50K/year), and you’ve upgraded your cash flow, tax-deferred. Great Point Capital’s Alternative Marketplace connects you to DST options, ensuring a smooth transition to passive rental riches.

Advanced Strategies to Maximize Rental Income

For accredited investors, a 1031 exchange isn’t just a tool to defer taxes—it’s a launchpad to supercharge rental income through deliberate, high-impact moves that go beyond basic property swaps. While trading a low-yield rental for a slightly better one delivers incremental gains, these advanced strategies harness the full power of tax-deferred reinvestment to catapult your cash flow to new heights. Whether you’re chasing double-digit rental streams, securing ironclad tenant revenue, or scaling up to multiply your income sources, these approaches elevate your portfolio’s earning potential. With the ability to preserve every dollar of your sale proceeds, you can strategically target properties that transform modest rents into robust returns, and Great Point Capital’s Alternative Marketplace provides the data and connections to execute with precision.

- Target High-Yield Markets: Exchange into growing regions (e.g., Austin, Charlotte) where rents outpace coastal averages—6–8% vs. 2–3%—to lock in superior rental income. These markets, fueled by population booms and economic growth, offer higher per-square-foot rents and stronger appreciation, making them ideal for cash-flow-focused investors. For example, swapping a $1M Los Angeles rental at 2% ($20K/year) for a $1M Austin multifamily at 7% ($70K/year) nets $50K more annually, tax-deferred. Research via Great Point Capital’s Alternative Marketplace for top performers, tapping into real-time market trends and property listings to pinpoint the hottest rental income zones before they peak.

- Focus on Tenant Quality: Buy properties with long-term, creditworthy tenants (e.g., medical offices) for reliable rental income that flows like clockwork, month after month. Stability trumps high but shaky rents—think a dental practice locked into a 10-year lease versus a trendy retail tenant prone to turnover, ensuring your cash flow withstands economic hiccups. A $1.5M medical office yielding 5.5% ($82.5K/year) from a rock-solid tenant beats a $1.5M apartment at 6% with spotty occupancy every time. This strategy minimizes vacancy risk and late payments, delivering rental income you can bank on, all secured through a tax-deferred 1031 exchange.

- Scale Up Units: Trade a single rental for a multifamily with 10+ units, multiplying rental streams—e.g., $2K/month to $20K/month—while spreading vacancy risk across multiple tenants. Instead of a $1M single-family home netting $24K/year (2%), exchange into a $1.5M 12-unit complex at $1,500/unit/month ($18K/month, $216K/year), slashing the impact of any single vacancy while boosting total rental income nearly tenfold. Larger properties also benefit from economies of scale—lower per-unit maintenance costs mean more of that rent stays in your pocket. It’s a tax-deferred leap from trickle to torrent, amplifying cash flow with every added door.

Rental Income Benefits Beyond the Numbers

While the immediate allure of a 1031 exchange lies in elevating your rental income from a trickle to a torrent, the advantages ripple far beyond just bigger monthly checks. For accredited investors, this tax-deferred strategy isn’t merely about chasing higher yields—it’s about building a rental portfolio that works smarter, not harder, delivering financial security and flexibility. These benefits amplify the cash flow gains, transforming your real estate holdings into a more efficient, resilient, and liberating income engine. By keeping your capital intact and targeting properties that optimize rental returns, you unlock a trio of perks that enhance both your bottom line and your peace of mind.

- Tax Deferral: Keep your full proceeds to chase higher rents, not pay the IRS, ensuring every dollar works toward boosting your rental income. For example, selling a $1.5M property with a $500K gain saves you $150K in taxes (at 30%), letting you reinvest the entire amount into a rental yielding $90K/year instead of settling for less after a tax hit. This preserved capital is the fuel for upgrading to properties with superior cash flow, compounding your rental earnings over time.

- Income Stability: Higher yields from better properties buffer economic swings, providing a steady rental income stream even when markets falter. A $1M rental at 6% ($60K/year) with reliable tenants weathers downturns better than a 2% ($20K/year) property prone to vacancies, offering a financial cushion for accredited investors. This stability means your cash flow remains predictable, letting you plan reinvestments or personal expenses with confidence.

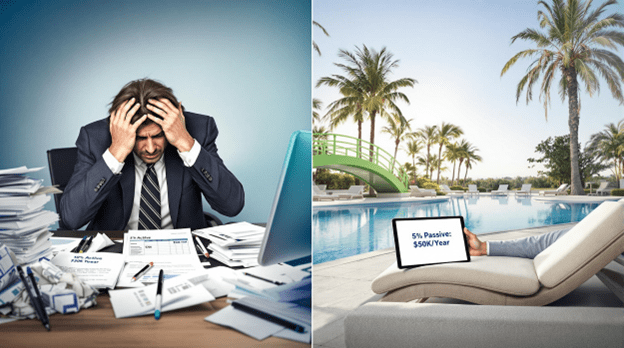

- Time Freedom: Passive DST rentals free you from landlord duties, boosting net income by cutting the hidden costs of time and effort tied to active management. Swapping a $1M active rental at 3% ($30K/year) for a DST at 5% ($50K/year) not only ups your rental take but eliminates tenant calls and repair headaches, effectively increasing your true return. For busy high-net-worth individuals, this hands-off approach turns rental income into a set-it-and-forget-it profit machine, enhancing both lifestyle and portfolio efficiency.

Pitfalls to Dodge When Upgrading Rental Income

Upgrading your rental income with a 1031 exchange promises a cash flow windfall, but the path is lined with potential missteps that can derail your gains if you’re not vigilant. Accredited investors, accustomed to managing substantial portfolios, know that precision is paramount—rushing or overlooking details can turn a rental income boost into a costly lesson. These pitfalls threaten not just your tax deferral but the very goal of securing higher, sustainable rents. By anticipating these traps and leveraging resources like the Great Point Capital Alternative marketplace, you can navigate the process with eyes wide open, ensuring your exchange delivers the rental income upgrade you’re after.

- Hidden Costs: A 7% gross yield might shrink to 3% net after expenses—vet thoroughly to avoid overpaying for a rental income mirage, focusing on net rental income, not headlines. For instance, a $1M property boasting $70K/year could lose $40K to taxes, insurance, and repairs, leaving you no better off than your old 2% rental—dig into operating statements before committing. Accredited investors should demand transparency on all costs to ensure the upgrade truly elevates cash flow.

- Market Missteps: Buying in a declining rental market risks income drops, undermining your goal of higher returns—use Great Point Capital’s data to pick winners with strong rental demand. A $1.5M rental in a fading industrial town might promise 6% today but crater to 4% as tenants flee, while a growing market like Charlotte holds steady or rises—research is your safeguard. This pitfall can turn a cash-flow dream into a rental income nightmare if you don’t prioritize market resilience.

- Deadline Pressure: Miss 45- or 180-day windows, and your rental upgrade incurs taxes, slashing the capital you need for a high-income property—plan with precision to keep your cash flow goals intact. A delayed closing on a $2M rental yielding $120K/year could force you to settle for a $1.7M option at $85K/year after taxes kick in, shrinking your upgrade’s impact—use tools like the Great Point Capital Alternative Marketplace to track timelines. For accredited investors, staying ahead of these deadlines is non-negotiable to maximize rental income potential.

Why 2025 is Prime for a Rental Income Upgrade

In early 2025, low-yield rentals face rising costs—interest rates, insurance, maintenance—making them cash-flow drains. A 1031 exchange lets you sell, upgrade to higher-rental-income properties, and defer taxes, capitalizing on growth markets. With Great Point Capital easing the shift, now’s the time to act.

A Typical Investor Scenario: Tripling Rental Income with a 1031 Exchange

Tom, an accredited investor, owns a $2M portfolio—two $1M rentals in LA yielding 2% ($40K/year total). In 2025, he sells, deferring $700K in gains, and uses a 1031 exchange via Great Point Capital’s Alternative Marketplace to reinvest: $1.2M into a Phoenix multifamily (6%, $72K/year) and $800K into a DST retail center (5.5%, $44K/year). His rental income leaps to $116K/year—nearly triple—tax-deferred.

Conclusion: Upgrade Your Rental Income Today

A 1031 exchange is your fast track to higher rental income, swapping low-rent duds for high-return stars, all tax-deferred. With Great Point Capital as your ally, the path is clear—start your exchange and unlock the cash flow you deserve.

FAQs

Swapping a 2% yield ($20K on $1M) for 6% ($60K) triples it—gains depend on your property picks and market conditions. With tax-deferred proceeds, you can reinvest the full amount into rentals with higher yields, maximizing your cash flow potential without losing capital to the IRS.

Yes—4–6% passive yields beat many active rentals’ 2–3%, with no management drag to erode your returns. DSTs, like a $50M multifamily stake accessed via Great Point Capital deliver steady rental income from institutional-grade properties, upgrading your cash flow effortlessly.

Match or exceed the debt on replacements to defer all gains, then target high-income rentals with the full proceeds intact. For example, replacing a $1M loan on a $2M sale with $1.2M in new debt lets you secure a property yielding $120K/year instead of settling for less after taxes.

Use Great Point Capital’s Alternative marketplace to scout high-yield markets and stable tenants—focus on net returns over gross promises. Its tools highlight regions like Austin or properties with long-term leases, ensuring your exchange targets rentals that truly boost cash flow.

If 6–8% is achievable, yes—every percent boosts your cash flow significantly, adding thousands annually to your income. For a $1M property, jumping from 4% ($40K) to 7% ($70K) via a tax-deferred 1031 exchange makes the upgrade a no-brainer for long-term gains.

Disclosures:

The content published on the 1776ing Blog is for informational and educational purposes only and should not be considered financial, legal, tax, or investment advice. The insights shared are intended to promote discussions within the alternative investment community and do not constitute an offer, solicitation, or recommendation to buy or sell any securities or investment products.